On this occasion, we spoke with engineer Tyrone Perdomo, who has extensive experience in crude oil marketing, delving into the paths that must be taken in Venezuela to maximize revenues from the sale of heavy crude oil and its relationship with its processing in the country. It is important to note that engineer Edgar Rasquin, former General Manager of the Paraguaná Refinery Center in Falcón state, contributed to the preparation of the answers, particularly with regard to questions 6, 7, and 8.

Possibilities and opportunities for the Venezuelan oil industry to place its crude oil production in markets that offer the best value for it.

1. Once democracy returns to the country, one of the main challenges it will face will be to rescue the markets for the sale of our crude oil. How difficult will it be to sell it, given that most of it currently comes from the exploitation of the Orinoco Belt and heavy crude from the west of the country, such as Boscán and Bachaquero 22?

Once the country returns to democracy and true, legitimate authorities are installed in public institutions, the Venezuelan oil industry will return transparently and formally to the international oil business.

The scenario envisaged under the new democratic government involves the full participation of local and international private investment in Venezuela’s oil industry.

Under this concept, a valid option is that the companies investing in crude oil production should also be responsible for its commercialization. All companies interested in investing in crude oil will be welcome, and their actions will be subject to contracts that include the corresponding commercial clauses.

These comments we are making today represent the case in which the marketing of crude oil produced in Venezuela is carried out by PDVSA or by the company designated by it.

It should be emphasized that all companies interested in purchasing crude oil will be welcome and subject to the commercial and administrative rules of the aforementioned company, which many of our colleagues in exile know in depth.

Venezuela has an extensive catalog of crude oils for sale: Boscán, Tía Juana Pesado, Laguna, Bachaquero, Menemota, Merey, Lagotreco, Mesa, Santa Bárbara, etc. The decision to sell volumes of one crude oil or another is the result of an analysis that takes several considerations into account. It involves recognizing the impact on the fuel production pattern of the refinery park as a system, compared to sales revenue. From what we understand of the situation of Venezuelan refineries, CRP and El Palito will consume all the light and medium crude oil available in order to operate the gasoline and diesel manufacturing units at a presumably stable level, which we understand to be in the order of 200 MBD in total.

As mentioned in the wording of the question, it is expected that the crude oils that will not be processed in Venezuela will be Boscán (9-10 API), extra-heavy crude oils from the Bolívar Coast (12 to 13 API), and crude oils manufactured with material from the Belt.

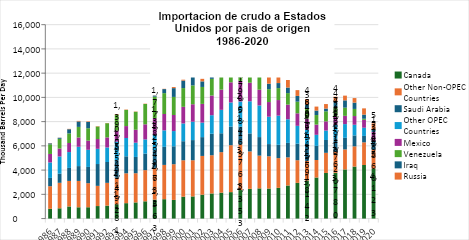

As a basis for our assessment, we can say that Venezuela was the largest exporter of crude oil to the United States in the mid-1990s. We are talking about almost 1.8 million barrels per day, most of which was heavy crude oil, due to the configuration of the Gulf refineries. This contrasts sharply with Venezuela’s current production of less than one million barrels per day.

Source: EIA and PDVSA internal records.

From our experience in selling Venezuelan heavy crude oil in the 1980s and 1990s, we can infer that the US market will be the preferred destination for the first barrels produced at the start and in the early years of the new government.

We can say that, given the installed capacity of Gulf refineries, their re-entry into this market has the benefit of improving refining margins for many components of this refining park. On this basis, we estimate that at least the first million barrels of heavy crude oil produced under the new administration will find a place in this cluster of refineries.

This impression is expressed despite competition from Canada, given the absence of competition from Maya crude (production decline) and Saudi Arabian crude in this market due to more favorable economies in the Asian market.

The difference between this initial phase and the current situation is that formal and transparent international market channels will be used, allowing sales on terms favorable to the country and exploring the most profitable markets without the need to seek out remote destinations, which would result in having to offer large discounts, in most cases fraudulent, to circumvent PDVSA’s commercial rules.

At a later stage, when we are producing higher volumes, say 3 million barrels per day, the strategy will be to place the incremental volumes at their best value.

2. What strategy would you propose to position Venezuelan crude oil in markets that value it most highly?

Diversification versus Market Purchase.

The story: Market Purchase

Since the early 1980s, PDVSA has carried out extensive campaigns aimed at placing the crude oil that would need to be produced in order to move from a company with a production of less than 2 million barrels per day to a company with a production of more than 3 million barrels per day. Those campaigns made it very clear to us that the market did not want our heavy barrels.

The decision: if the market won’t buy my barrels, we’ll buy the market, and that’s what we did.

By doing so, with some tailwinds (light winds from Monagas) and without much financial capacity, PDVSA managed to produce 3 million barrels in 1995, more than half of which were heavy crude produced in the last ten years.

These campaigns in Venezuela, together with those in Mexico and Canada, left behind a legacy of a structure capable of processing heavy crude oils, highly contaminated with sulfur and metals, as well as high levels of corrosivity in the Gulf refining park.

In recent years, this capacity has been underutilized due to the lack of availability of heavy crude oils, mainly from Venezuela and Mexico.

Market purchases enabled PDVSA to grow to 3 MMDB, mainly based on increased production of heavy crude oil.

Source: Data taken from own files from work at PDVSA.

As stated in the answer to the question above, the placement of, say, the first million barrels to be produced under Venezuela’s new administration could be favorably placed in contracts or bids with refineries in the Gulf of America.

The outlook: Market diversification

At some point after a certain level of exports to the Gulf, it is conceivable that incremental volumes would begin to be competitively on par with placements to India and China. This economic law of diminishing returns as activity grows, which could be found at some stratum of our production level, could be counteracted through creative diversification of markets, exchanges, and trading. This degree of freedom or flexibility in our heavy crude oil placements, which did not exist in the 1990s, is now a real possibility.

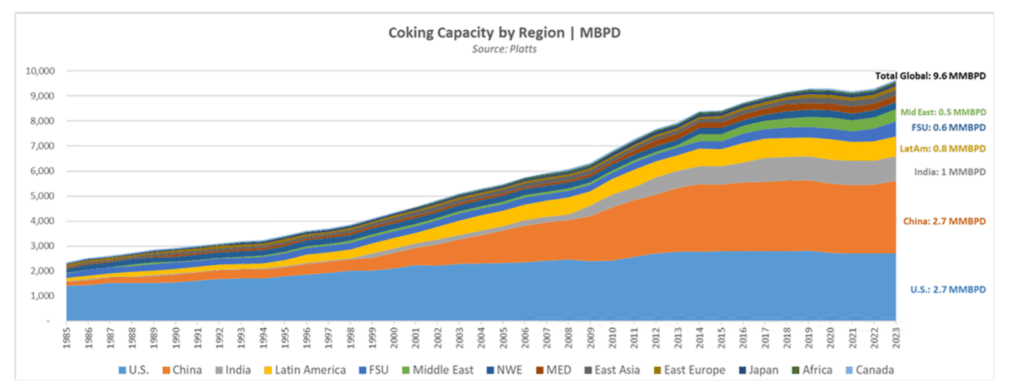

As can be seen in the graph below, the configurations of many refineries in Asia have changed significantly. In the late 1990s, we were confined to selling our barrels only in PAD III in the United States.

This was because the capacity to process heavy crude oil economically was located only in this part of the world.

Now we will find a clientele capable of refining them on the other side of the world. This is reflected in the evolution of coking capacity in countries such as India and China.

Environment for heavy crude oil exports in a democracy

Evolution of Deep Conversion Capacity worldwide

Source: EIA and PDVSA internal records.

Given this situation, and faced with a pluralistic world for the placement of Venezuelan extra-heavy crude oil, possibilities are being considered to add value through creative negotiations based on negotiation schemes where the currency to be explored is the option to place barrels in other markets.

Crude oil segregations that make economic and commercial sense would be maintained for incorporation into the market and in accordance with the interests of buyers. That is, segregating light, medium, and heavy crude oils to seek placement for each according to its quality, in order to maximize benefits for the country.

3. Venezuela is producing volumes of light crude oil in both the west and east of the country. This crude oil is being used to blend with bitumen from the Orinoco Belt and marketed as Merey 16, and for processing in the country’s refineries to produce jet fuel, gasoline, and diesel. Would you change this current strategy? Please explain.

This question brings us to the mechanical aspect of heavy crude exports.

Currently, higher-value light crude is being degraded so that it can be mixed with heavy crude and bitumen from the Belt and marketed as Merey 16 crude.

This way of working is due to the lack of operability of Jose’s Strategic Partnerships’ upgraders, which forces the incorporation of light crude oils to produce marketable crude oil.

As long as the upgraders remain in the same condition, we must evaluate the possibility of finding a mechanism that will allow us to efficiently, i.e., economically, replace the current practice of degrading light crude oils to blends.

This exercise, which is already being carried out in Colombia with the production of extra-heavy crude oil in the Eastern Plains of that country, consists of determining the availability in terms of volumes and prices of diluents that:

- Enable efficient handling of crude oil from the Belt during transport by ship.

- Represent a marketable material to a significant number of refiners in the corresponding volumes.

- Represent a better economic return for the nation.

In my view, these economic assessments and market considerations can be initiated very early on by taking advantage of PDVSA’s existing infrastructure abroad (CITGO) and/or making use of Commerce personnel in exile.

4. Do you believe that the country’s refineries should continue operating and producing fuels as they do now, thereby exporting more crude oil, including the light crude that is currently processed in those refineries?

An analysis of current activities will reveal the availability of crude oil and products at the national level. The balance between the products of refineries currently in operation and the country’s needs will determine the import requirements to meet that demand.

That is the base case. The volumes of crude oil that are determined not to be sent for refining will be sold.

Plans are in place to restore refining infrastructure by bringing private companies, both domestic and international, into the refining business. The objective is to generate economic incentives to encourage these private entities to invest in existing refineries, in accordance with their operational infrastructure. These incentives could come from innovative contracting schemes that integrate the entire oil value chain and represent opportunities for contracting companies.

For example, refineries are identified that could be operated by transnational companies that have the technology, know-how, and markets to make them a profitable and attractive business. This group includes the El Palito and Puerto la Cruz refineries, which have the infrastructure to process light and medium crude oils.

On the other hand, the Paraguaná Refining Center (CRP) could also participate in these new contracting schemes. Given its size, capacity, and versatility, more complex business and investment schemes are envisaged, such as the partial conversion of the CRP into a heavy crude oil upgrader for the Orinoco Belt, among other options that may be of interest to private companies.

In addition to the need to restore the refining facilities, there are also plans to rescue the existing petrochemical infrastructure and promote new businesses in the refinery sector, which may offer investment opportunities to third parties specializing in this sector. This proposal could lead to the creation of new companies and revive the country’s petrochemical and chemical sector. This is a gold mine of opportunities that PDVSA was promoting 25 years ago, but this regime destroyed the incentives by nationalizing or simply ignoring all initiatives.

5. PDVSA’s commercial management is unsuccessful because it relies on non-transparent transactions to export its crude oil. What changes do you propose to, first, maximize revenue for the nation, and second, manage the transition from one business model to another?

Clearly, PDVSA’s current management is riddled with malpractice, non-compliance with commercial, administrative, and operational procedures, and irregular and corrupt handling of the business’s accounts and funds.

To eliminate the aforementioned deviations, it will initially be necessary to implement or reinstate rules governing the organization’s operations and establish auditable procedures. Likewise, it is necessary to incorporate an organizational culture that involves a change in attitude and generates the necessary commitment of the people to the company.

However, as the industry expands with the participation of private companies, the oil business will take on its own character under the policies of the various private companies that will take over its management.

6. What recent disruptive technologies have been incorporated into the industry to optimize refining efficiency and minimize environmental emissions?

An issue that is always present in the environmental performance of the oil industry, and in particular the refining sector, is its impact on emissions and discharges into the environment.

Although most conventional refining heaters still run on fossil fuels (natural gas or fuel oil), there are advances associated with the alternative use of renewable energies to generate electricity for heating equipment that show a clear trend and potential for change. Some specific applications in refining and petrochemicals:

For refining heaters (preheaters, boilers, combustion heaters), electrification is being considered as a means of decarbonization: for example, replacing gas heaters with electric or induction heaters in certain units.

All our refineries have old equipment, and investors may have incentives to modernize them: replacing four large combustion heaters with electric equivalents (as projected in a study).

This change supports broader efforts to decarbonize refineries, including reducing direct emissions, increasing process flexibility, using renewable energy, and enabling modular upgrades.

On another note, new technologies are being developed to minimize emissions and reduce the carbon footprint. Among them is Carbon Capture and Storage technology. This technology allows carbon to be captured in the form of CO2 after combustion and transported to underground formations where it can be injected to improve reservoir production or simply stored in depleted wells.

However, in addition to new technologies, it is important to ensure that existing and proven technologies that reduce environmental impact are operated properly and efficiently to minimize emissions and discharges, such as acid gas treatment and separation plants, sulfur recovery, acid water/process water treatment, gas recovery systems at the cinder bed, etc.

Likewise, emergency systems in case of fire will be evaluated and audited, such as the firefighting water system, portable extinguishers, sprinkler systems in plants, and foam systems in tanks, as well as equipment and systems for controlling spills on land and in water bodies.

7. Human safety and environmental protection are priorities. What are the most effective risk management strategies that have been implemented to ensure safer refining operations and minimize environmental impact?

Indeed, safety and environmental protection are essential components of oil business management. These have been neglected to such an extent that accidents, fires, and spills have increased significantly and constitute an issue that requires immediate intervention at the time of transition.

This will be one of the issues that needs to be addressed from the outset. In this regard, the Emergency Tactical Plan, which has been prepared to address initial entry into the refining facilities, provides for inspections and audits of the condition of the process units and infrastructure. The objective is to determine the current condition and risks associated with the operation in order to decide whether it is safe to continue the operation or to shut it down.

8. Beyond fuels, refining is a social pillar. Could you elaborate on the critical impact of refining by-products on other industries (such as petrochemicals and pharmaceuticals) and their contribution to society? (It is estimated that thousands of derivative products are generated.)

The recovery of the refining sector and, in general, of the oil industry, will directly and indirectly generate economic growth and, therefore, the creation of skilled and unskilled jobs in many areas, in addition to the oil industry. The participation of private companies in all business activities will have a significant multiplier effect, because it will no longer be just the state acting alone, but a large number of private actors participating in the generation of industrial activity.

As the oil industry’s infrastructure recovers and expands into unconventional areas of the industry, such as petrochemicals and related industries, the industry’s growth will drive the recovery of the country’s economic and social fabric and strengthen wealth creation.

This will enable Venezuelans to find jobs with adequate pay to provide their families with a decent life.

The views expressed by Tyrone Perdomo are of his personal ownership and responsibility, and do not necessarily reflect the position of PDVSA Ad Hoc.